A few years ago, most businesses treated money movement as a feature they could plug in later.

That is no longer how the market works.

Today, if you are building a fintech product, a wallet, a payroll platform, a remittance service, or even a commerce ecosystem with embedded finance, the ability to move money smoothly is part of the core product itself.

People no longer compare your product only with direct competitors. They compare it with the easiest payment experience they had anywhere that week. If sending money on one app takes a few taps, but your platform makes people struggle through forms, delays, and unclear status updates, trust drops immediately.

This is why how to build a money transfer app is not just a product question. It is a business question.

In practice, building a transfer app means answering some questions very early.

For example:

So before we get into build steps, cost, and architecture, it helps to first get clear on the basic shape of the product itself.

Also read: Mastering Payment Gateway Integration for Your Site

A money transfer app is a digital product that lets users send, receive, or manage the movement of money through a mobile or web interface.

That sounds obvious, but it is worth defining properly because not every payment app is the same.

At a basic level, a money transfer app usually allows a user to:

The transfer itself may happen through different mechanisms.

It might use a bank account, a card, a prepaid balance, a real-time payment rail like UPI, or even a cross-border partner network such as SWIFT-based banking infrastructure for international transfers.

That is why a money transfer app is really a product layer sitting on top of a payment system.

In the Indian context, that distinction matters even more.

The Payment and Settlement Systems Act treats payment systems as formal infrastructure, including systems involved in money transfer operations. So when a company says it wants to build a transfer app, what it is often really saying is that it wants to build a user-facing layer on top of regulated payment movement.

That user-facing layer can look very different depending on the business model.

For example, Google Pay and PhonePe feel simple to consumers, but their simplicity is made possible by a deeper ecosystem involving NPCI, PSP banks, TPAP roles, authentication flows, and bank connectivity. NPCI’s UPI framework explicitly sets out roles and responsibilities in that system.

This is where many teams make an early mistake. They think of the app as the product. In reality, the app is only the visible part of the product.

Underneath it, you usually need:

So when someone says they want to create a money transfer app, I usually break that into a clearer question.

Do they want to build:

Each of those is a different build in practice.

Also read: An end-to-end Guide to Stock Trading App Development

Not all transfer apps solve the same problem, even if the user action looks similar on the surface.

That matters because the type of app you choose will affect everything that comes later, including features, compliance, integrations, timeline, and cost.

This is the model most people now recognize instantly. One user sends money directly to another. In India, this often happens through UPI-linked apps. In other markets, the closest mental models are products like Venmo or Cash App.

This type works well when the goal is speed, frequency, and convenience.

Here, the app is closely tied to a banking relationship. Instead of acting like a lightweight payment layer, it works more like an extension of banking infrastructure. Transfers may run through bank accounts, direct bank rails, or tightly governed partner flows.

This model is common when trust, compliance, and account-level control matter more than lightweight consumer growth.

In this model, users may store value inside the product and use that balance to send or receive money. This can make the user experience feel faster and more contained, but it also introduces additional questions around stored value, settlement, and regulatory structure.

This is where complexity rises quickly.

Now you are not just moving money between two users. You are dealing with a lot of complexity such as:

That is why a domestic UPI-led product and a remittance-led product may both look like transfer apps, but they are very different businesses under the hood.

The important thing is to choose the type based on the real use case, not on what looks attractive from the outside.

So once the app type is clear, the next question is: How do these apps actually move money in the real world, and what has to happen between the user tapping “send” and the payment reaching the other side?

Also read: Augmented Reality in Banking: Future of Financial Services

From the outside, a money transfer app is very simple.

A user opens the app, enters an amount, selects a recipient, confirms the payment, and gets a success message.

But under that simple moment is a sequence of systems working together in real time or near real time.

If you are planning money transfer app development, this is the point where the project becomes real. You stop thinking about screens and start thinking about flow.

In most cases, the flow looks like this:

1.The user logs in and is authenticated

2.The app checks whether the user is allowed to make the transaction

3.The payment instruction is created

4.The app sends that instruction to the relevant rail or partner system

5.The system receives a success, failure, or pending response

6.The app updates the transaction status and notifies the user

Let me make that a bit more practical.

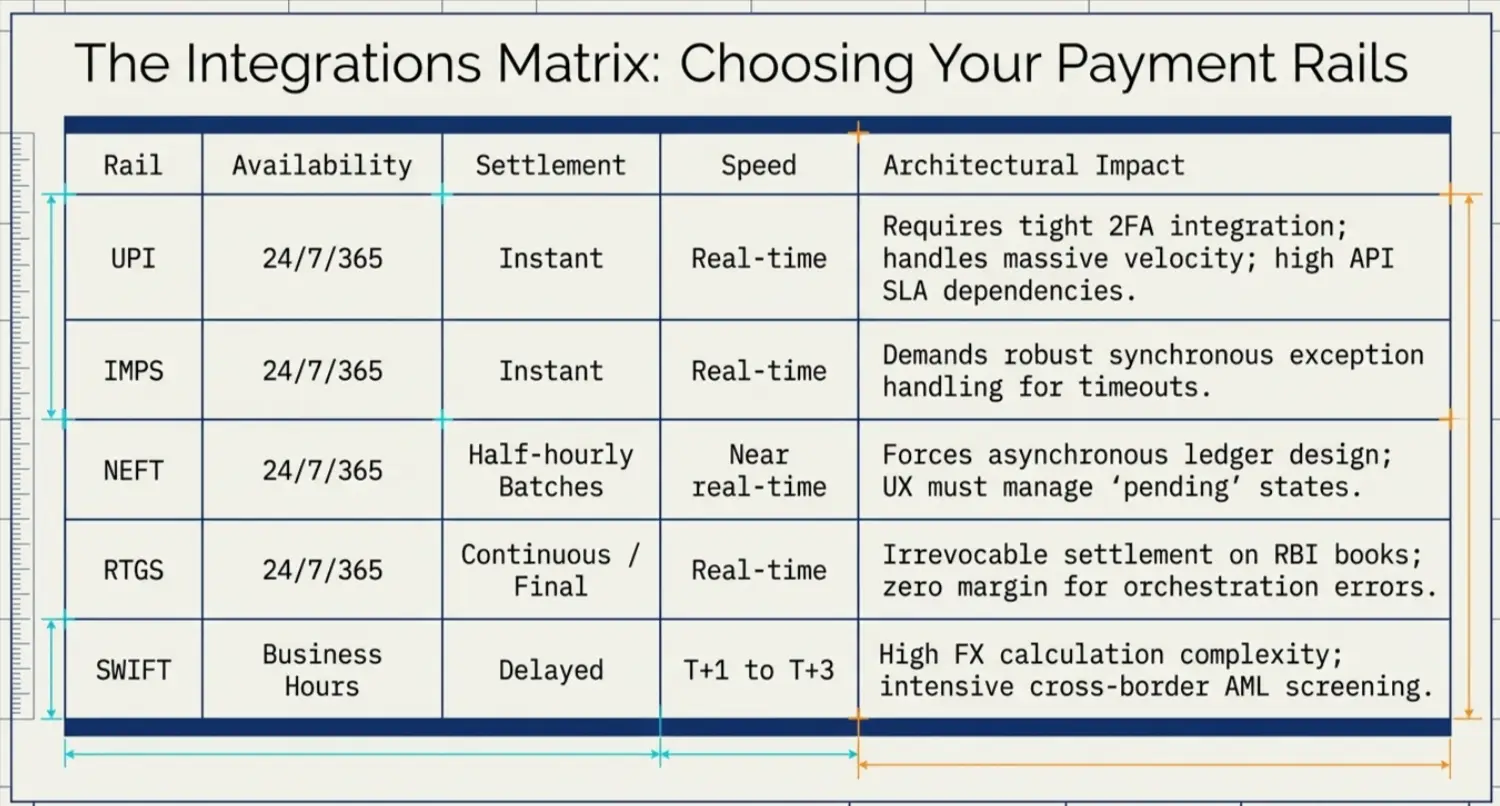

If the app is built for India and uses UPI, the payment is moving through an ecosystem defined by NPCI, PSP banks, and TPAP roles. NPCI describes UPI as a real-time payment system that enables bank-to-bank payments on a 24x7 basis.

If the app uses NEFT or RTGS rails through bank integrations, the behavior changes. RBI notes that NEFT works 24x7 in half-hourly batches, while RTGS is real-time and final.

This difference matters, because the user may see one simple “Send Money” button, but the system behind that button may behave very differently depending on the rail.

Here is a clean way to look at the moving parts:

This is where weaker products break, not because the payment cannot be initiated, but because the app cannot handle what happens around the payment.

Serious online payment transfer app development effort needs more than just API integration. It needs a proper transaction lifecycle.

In practice, that lifecycle should answer questions like:

This is also why the internal ledger matters.

Even if the product is not a wallet in the formal sense, the system still needs an internal record of what was initiated, what was acknowledged, what settled, and what reversed. Stronger competitor pages now mention ledgers and settlement states, but most still do not explain their day-to-day impact on the product experience.

If the status model is weak, customer support becomes weak.

If reconciliation is weak, finance teams lose confidence.

If duplicate handling is weak, trust drops.

So when people ask me how to build a money transfer app, I think this is one of the most important answers: build the flow before you polish the interface.

Also read: E-commerce Digital Transformation

For a first release, these are the core features I would treat as non-negotiable in build money transfer app projects:

Then there are the business-side features, as a transfer app is not only a consumer product. It is also an operations system.

That means the admin side needs features like:

Without these, the product may look polished from the outside but become painful to operate internally.

For example:

But these should come after the base product is stable, because a transfer app does not become valuable by having more features.

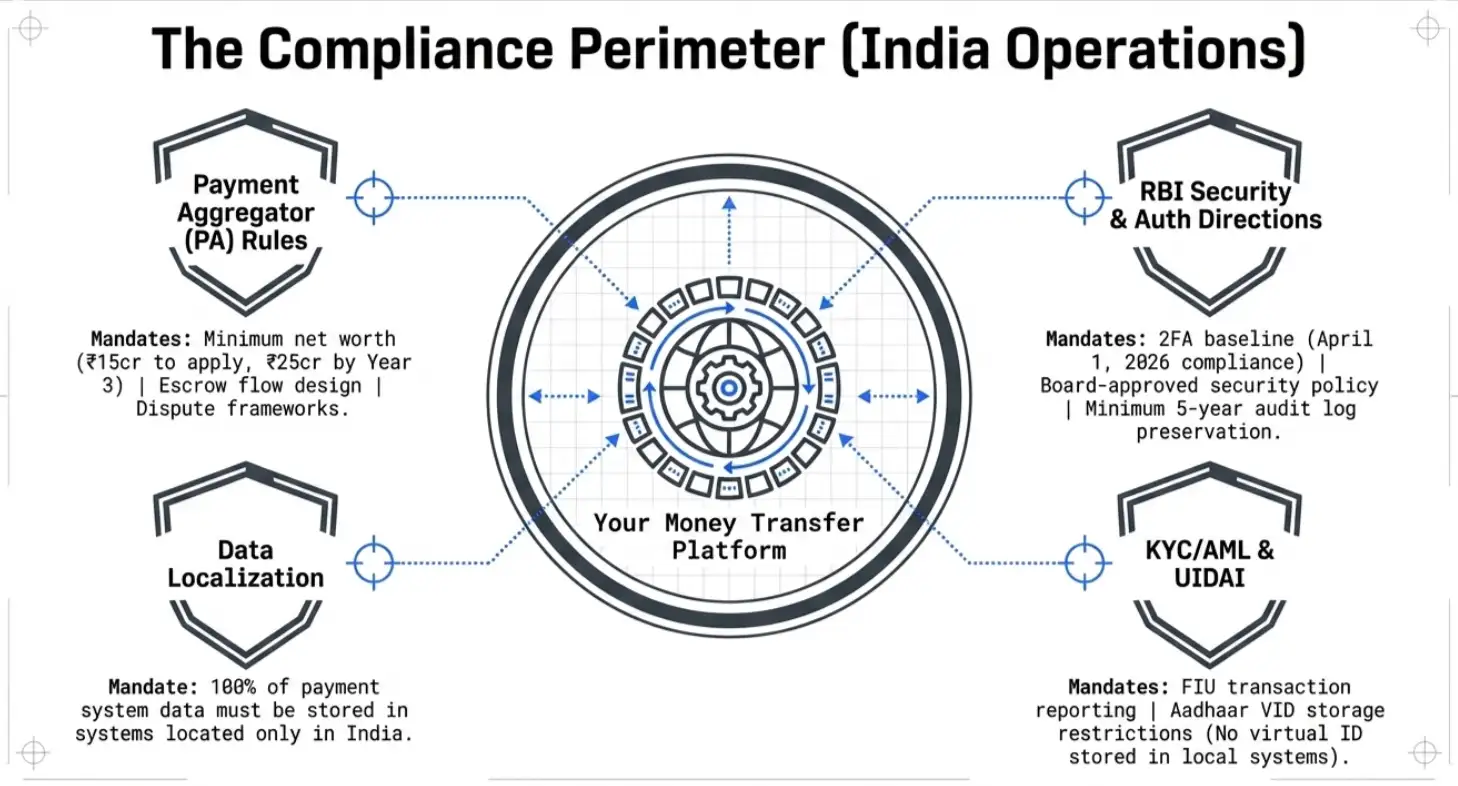

If you are building a transfer app for India, compliance cannot sit in a legal folder while product and engineering move ahead separately.

At the highest level, you are working inside a payments environment governed by RBI, with rails and participation models influenced by entities like NPCI for UPI. The legal perimeter around payment systems in India is set by the Payment and Settlement Systems Act, and RBI’s directions and master directions shape how regulated participants and operators are expected to function.

For a practical build, there are four areas that matter most.

If users are moving money, you need a reliable identity process. That usually means some combination of:

RBI’s KYC framework goes beyond simple onboarding. It includes customer identification, due diligence, beneficial owner identification, and record management.

Money movement products need anti-money laundering controls.

That means the system should be able to detect and flag unusual behavior, and the operating team should be able to investigate it.

In practical terms, this means having controls around:

FIU-IND’s framework around record maintenance and reporting reinforces that this is not optional for relevant participants.

RBI’s 2025 directions on authentication mechanisms for digital payment transactions reinforce the requirement for two factors of authentication, with compliance expectations in place by April 1, 2026 for covered participants.

So your product needs a clear approach to:

RBI’s payment system data localization direction requires payment system data related to operated systems to be stored in India.

That affects:

So if I had to put the India picture in one simple line, it would be this:

A money transfer app in India is a regulated movement-of-money experience that must align product design, identity, security, and data handling from the start.

And once that compliance foundation is in place, the next decision becomes more technical.

Once the product flow is clear and the compliance boundary is understood, the next question is — What should the app be built on?

I separate stack decisions into four layers.

For mobile products, teams choose between:

If speed to market matters and the initial feature set is well scoped, cross-platform makes sense.

If the product needs deep platform optimization, heavier device-level security controls, or highly tuned user experience, native can be the better route.

The right choice depends less on ideology and more on the product stage.

A transfer platform backend usually needs services for:

For this layer, common technology choices include Node.js, Java, and Python.

Node.js is chosen for fast iteration and event-heavy systems.

Java is preferred where teams want strong enterprise controls and mature large-scale reliability.

Python is useful in surrounding layers, especially if analytics or fraud models are involved.

The bigger decision is not language but architecture.

Should you begin with a monolith or microservices?

For an early-stage product, a modular monolith is often the smarter answer.

It is simpler to build, easier to test, and faster to manage.

Microservices make more sense when the product has reached enough scale that separate transaction, risk, notification, and admin domains genuinely need to evolve independently.

This part needs more care than most teams expect.

A payment app is one where you are storing transaction truth.

That usually means:

This is where the ground reality matters.

If a user says money left their account but the recipient did not get it, your system has to answer that question clearly.

That is why the data model needs to represent states like:

Without that, the product becomes hard to operate as soon as volume grows.

A transfer app is rarely a fully isolated product.

It connects to:

In India, if the app is connected to UPI-style flows or bank-linked transfer systems, the integration layer needs to be built with resilience in mind because network, partner, and callback behavior are not always perfectly clean in production.

emember that the best architecture is not the most complex one.

It is the one that keeps the product understandable while making growth possible.

And once that architecture is outlined, the next step is execution.

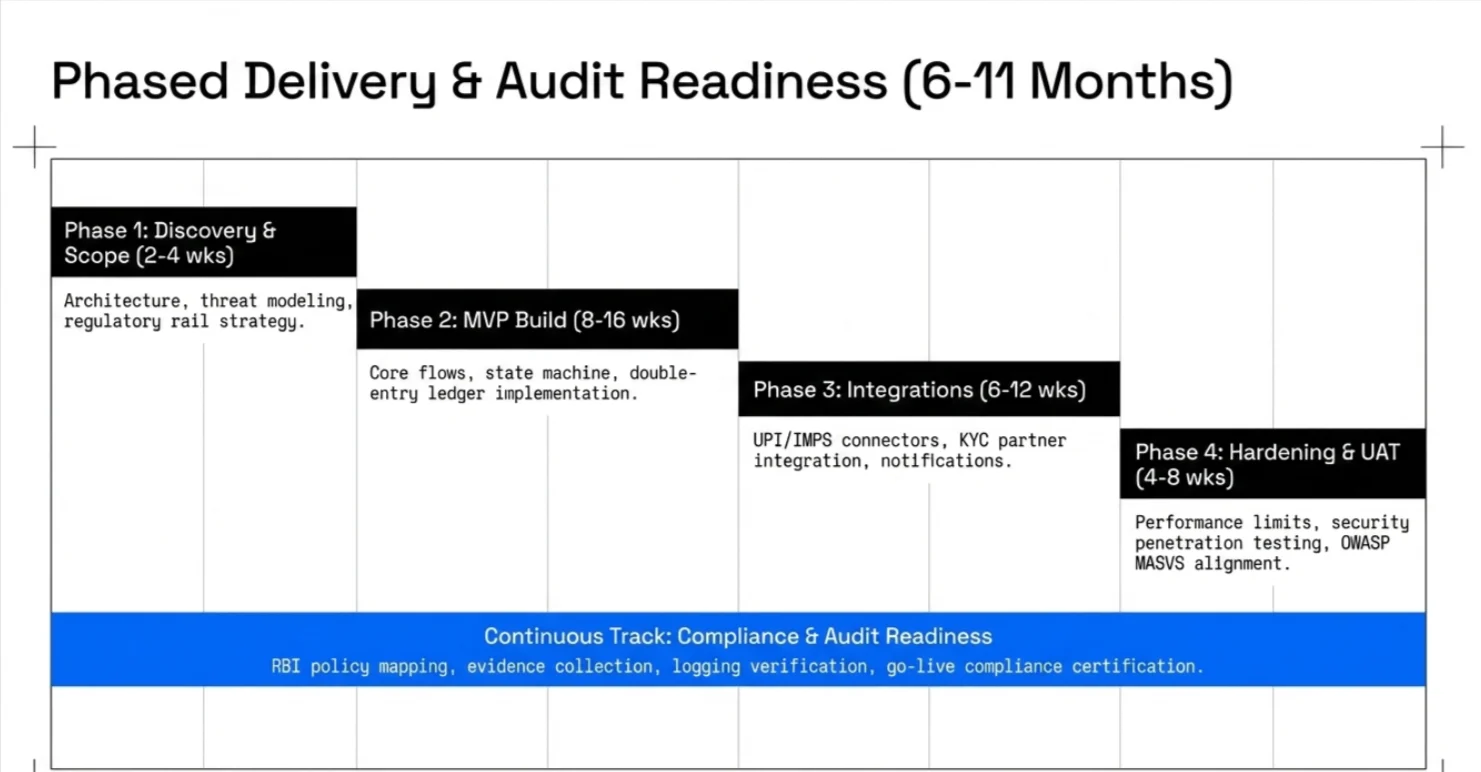

This is the process I find most useful in real-world builds.

Start by deciding what problem the app will solve.

Is it:

This decision shapes everything that follows.

Next, decide how money will move.

Will the product use:

At this stage, product ambition needs to meet real payment infrastructure.

Before design gets too far, the compliance scope should be clear.

This includes:

This step often saves months later.

A good MVP is not the smallest possible app.

It is the smallest version that proves the money movement experience end to end.

That usually means:

This stage focuses on making the product feel simple.

That usually involves simplifying:

If users do not understand what happened to their money, the experience is broken even if the transaction system worked correctly.

Now the system is developed.

This includes:

This is where architecture quality begins to show.

Payment products need more than UI testing.

They need:

Because real users do not behave like demo users.

A staged launch is usually better than a full public launch.

Start with:

The first post-launch questions are usually not about design.

They are about:

The cost question is always important, but it becomes more useful when framed the right way.

The wrong question is:

“How much does a transfer app cost?”

The better question is:

“What drives cost in a transfer app?”

Because the answer depends less on the number of screens and more on the complexity underneath.

The biggest cost drivers are usually these:

A simple domestic MVP is very different from a multi-rail product with advanced fraud controls and enterprise reporting.

That is why the range in the market is wide. Competitor and agency benchmarks commonly show broad bands, from modest MVP budgets to much larger enterprise builds depending on feature depth and compliance scope.

These are planning ranges, not fixed quotes.

In many cases, maintenance is also a meaningful line item. Some agency guidance estimates annual maintenance at around 15 to 20 percent of initial build cost, though real numbers depend on usage, integrations, and operating complexity.

There is also a very real location and team model effect.

A product built with a tightly aligned partner in India will often have a different cost structure from one built through a large Western delivery model.

By the time a business reaches this stage, the challenge is not understanding that the opportunity is real. The harder part is deciding how to turn the idea into a product that works on the ground, not just in a slide deck.

This is where I believe the role of a technology partner becomes practical, not promotional.

A serious money transfer app development initiative needs alignment across:

At Neuronimbus, that is how we approach this category.

We do not look at a money transfer app as just another app build. We look at it as a connected system where the user journey, transaction flow, controls, and support model all need to make sense together.

The important point is that the build has to be grounded in real usage.

If you want to know how to build a money transfer app, the answer is not one tool, one framework, or one shortcut.

It is the discipline of getting the flow, architecture, controls, and user experience to work together.

And when that happens, the product does not just launch, it holds up.

If you're evaluating a money transfer app build, we're happy to start with a no-commitment discovery conversation.

Start your free assessment with the Neuronimbus team.

A money transfer app enables users to send, receive, and track money movement. Unlike general payment apps, it acts as a layer on top of regulated payment systems like UPI, bank rails, or SWIFT.

Core features include user onboarding (KYC), secure authentication, bank or payment source linking, transaction flow, real-time status updates, and admin tools for monitoring and reconciliation.

Apps in India typically use UPI, NEFT, RTGS, or wallet systems. The choice depends on speed, use case, compliance requirements, and whether the app supports domestic or cross-border transfers.

Costs vary widely. A basic MVP can range from $40,000 to $120,000, while advanced or enterprise-grade platforms can exceed $300,000 depending on complexity, integrations, and compliance scope.

The hardest parts are not UI—they are handling transaction failures, retries, reconciliation, compliance (KYC, AML), and ensuring a clear, reliable payment status for users and operations teams.

.webp)

Let Neuronimbus chart your course to a higher growth trajectory. Drop us a line, we'll get the conversation started.

Call Us

Schedule a Call

Your Next Big Idea or Transforming Your Brand Digitally

Let's talk about how we can make it happen.