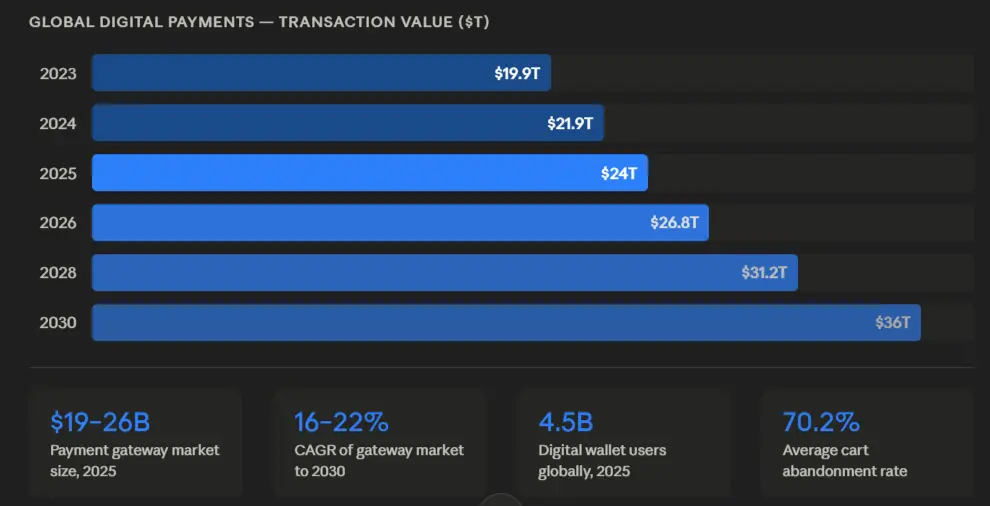

In 2025, the world moved $24 trillion through digital payment systems.

By 2030, that number will reach $36 trillion.

The payment gateway market is growing from $19 billion today to somewhere between $40 and $132 billion by the end of the decade, depending on whose projections you use.

That kind of growth signals that payment gateway development has moved from a technical decision to a strategic one.

The companies that understood this early are now in a different position to everyone else.

Let’s take the best example. Shopify built its own payment infrastructure. In 2024, Shopify Payments processed $180.9 billion in gross payments volume, which is 62% of Shopify's total GMV, and became the company's single largest revenue driver.

So if you're a CTO or IT leader reading this, every time a customer pays you, one of two things is happening. You're building equity in your own payment infrastructure. Or you're paying rent to someone else's.

This guide is about understanding when to stop renting, and what payment gateway software development actually involves.

Also read: Mastering Payment Gateway Integration for Your Site

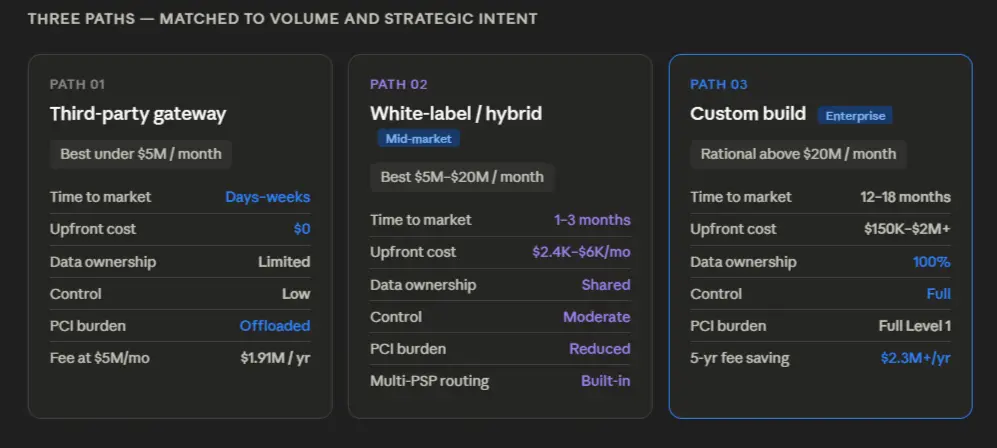

Most custom payment gateway software development playbooks frame this as a binary. Build a payment gateway or buy one. That framing is too simple, and it leads to the wrong decision in the middle of the market.

If you're processing under $5 million a month, third-party gateways are almost certainly the right answer. All major ones like Stripe, Adyen, Braintree, Checkout.com, Razorpay, PayTabs are fast to deploy, require no upfront capital, and handle PCI compliance for you. You're live in days to weeks.

The trade-off becomes visible at scale.

Fees compound significantly as volume grows. Your transaction data stays in the provider's black box. Your checkout experience is limited to what they allow. And when new payment rails emerge in your markets you wait for their product roadmap, not yours.

Below $5 million a month, those trade-offs are acceptable. Above it, they start costing you.

This is the payment gateway software development path most decision-makers don't consider seriously enough, and it's often the smartest move for businesses in the $5 million to $20 million a month range.

Providers like Corefy, Akurateco, and IXOPAY give you a branded checkout experience, multi-PSP routing out of the box, and deployment timelines of one to three months rather than twelve to eighteen. Payment orchestration layers like Primer and Spreedly sit above multiple PSPs.

These are not second-best options. Adyen for Platforms processes over $800 billion annually. Marqeta powers the card infrastructure for Square, DoorDash, and Klarna.

You get meaningful control over data and checkout experience, without the full capital commitment and compliance burden of a custom build.

Above $20 million a month, the financial case for a custom build becomes hard to ignore.

At that volume, the gap between custom infrastructure at around 2.0% all-in and Stripe's standard rate of 2.95% is approximately $2.3 million a year. A $500,000 build pays for itself in under three months at that volume.

One honest caveat: negotiated Stripe enterprise rates around 2.3% narrow that gap considerably. Fee savings alone rarely justify the build at that point. The stronger argument is strategic, that is, owning your transaction data, controlling your checkout experience end to end, and having the architectural flexibility to move into adjacent financial services or support new payment rails without waiting for a vendor.

Also read: An end-to-end Guide to Stock Trading App Development

A production payment gateway has several core components. Four of them carry serious strategic risk if they're built poorly.

On the broader architecture pattern: a monolith is cheaper to build initially. It's also a ceiling. Microservices with event-driven architecture means a fraud engine failure doesn't bring down checkout, and a routing outage doesn't affect settlement. PCI DSS scope narrows to specific services rather than the entire system. If you expect to process more than $10 million a month within 24 months of launch, microservices is not optional.

Most tech stack conversations go deep into languages and frameworks. That's not what matters at this level. What matters is three foundational decisions that carry business consequences.

Where your data lives. Your transaction ledger needs a database that cannot lose or corrupt a record under any failure condition. That's a non-negotiable constraint, not a preference.

Where your encryption keys live. Cloud-hosted key management removes significant upfront hardware cost but creates dependency on your cloud provider. On-premise gives you full control. This is a capital versus operational cost decision — and a regulatory one in markets like India and the UAE where data localisation rules apply.

How your system communicates internally. An event-driven architecture with an immutable message log means every transaction event is recorded in sequence and cannot be altered. That's not an engineering preference — it's your audit trail, and regulators will ask to see it.

From the moment a customer clicks pay to the moment funds settle in your account, a transaction passes through fifteen handoffs. Most of them are invisible to the customer. A few of them are architectural decisions with direct consequences for your revenue.

How you handle card data at the point of entry determines the scope of your entire compliance programme.

How you tokenise that data determines your authorisation rates and your interchange costs.

How you authenticate the transaction determines your checkout conversion.

And how you route the payment determines whether a single acquirer outage takes your whole system down or just triggers an automatic failover.

The target for all of this end to end: under 300 milliseconds. That's the difference between a checkout that feels instant and one that feels broken.

On availability, the number that focuses the mind is this: a gateway processing $20 million a month loses $27,700 for every hour of downtime, before you account for customer churn or reputational damage. That's why high availability is a revenue protection decision.

The architecture you build determines your compliance burden as much as your technical capability. Which is exactly where we need to go next.

Also read: Augmented Reality in Banking: Future of Financial Services

Architecture gets you the foundation. Features determine whether the thing you built can actually compete.

Cards, digital wallets, BNPL, real-time rails specific to each market (UPI, FedNow, Faster Payments, AANI) and emerging settlement rails like stablecoins — the landscape keeps expanding, and your gateway needs to keep up with it.

The architectural principle that matters: payment method support must be additive. If adding a new rail requires a core system change and a three-month sprint, your architecture is behind where the market is heading.

Global payment fraud cost $442 billion in 2025. AI-enhanced fraud is now 4.5 times more profitable than traditional methods. A production fraud architecture runs at three layers simultaneously: a fast rules engine for deterministic checks, an ML scoring layer trained on your own transaction patterns, and a manual review queue for edge cases.

Multi-acquirer routing is the feature most organisations underestimate until something fails. A 2% improvement in authorisation rate at $20 million a month in volume is $400,000 in recovered monthly revenue.

Soft declines are instances where the card isn't actually blocked, just temporarily declined. These represent 70 to 90% of all failed card-not-present transactions. Smart retry logic recovers up to 70% of those. No retry logic means that revenue is simply gone.

Real-time dashboards showing authorisation rates, decline codes, and settlement status. Automated reconciliation that moves from exact matching to fuzzy matching to manual review queue. Merchant onboarding automation that compresses what used to take weeks into hours.

These are the features that determine daily operational reality for the teams actually running the system.

PCI DSS Level 1 compliance baked in from day one. HSM-based key management, network tokenisation, scoped card data collection so raw card data never touches your application servers, and TLS 1.3 as the minimum standard for data in transit.

Also read: E-commerce Digital Transformation

The regulator you operate under determines your data infrastructure, your capital requirements, your infrastructure geography, and your realistic timeline to market.

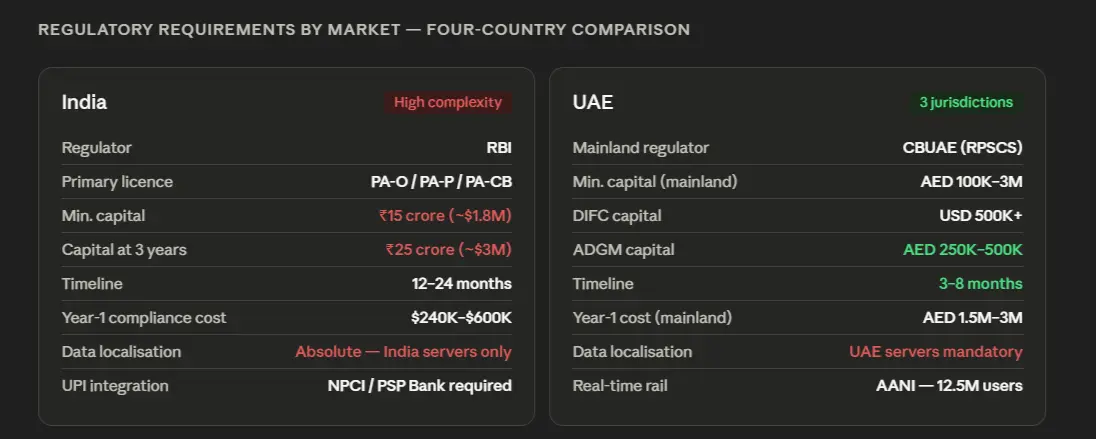

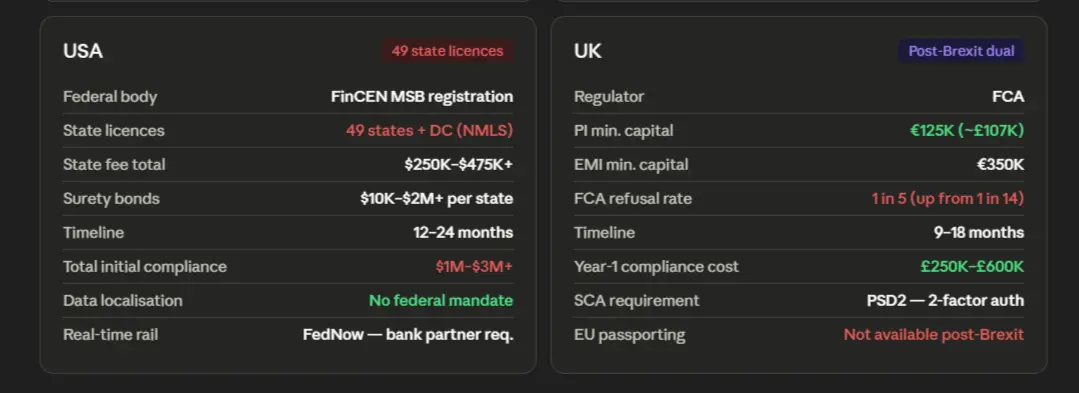

India centres on the RBI Payment Aggregator licence — three categories covering online (PA-O), physical (PA-P), and cross-border (PA-CB), each requiring separate authorisation.

Data localisation is absolute. All payment system data must reside on Indian servers. RBI enforced this against Mastercard in 2021, barring them from new domestic onboarding. Your cloud must be AWS Mumbai, Azure India, or GCP Mumbai. Mandatory quarterly internal VAPT and annual external VAPT. The DPDP Act 2023, with rules notified November 2025, adds penalties up to ₹250 crore.

The UAE has three distinct regulatory environments.

Data localisation under CBUAE is mandatory. All consumer and transaction data must be held within the UAE, with a separate UAE-based backup. AANI integration is the expectation for any gateway operating in this market, not an optional add-on.

The USA has no federal payment gateway licence, which sounds simple until you discover that 49 states plus DC each require Money Transmitter Licences through NMLS. Direct state fees for nationwide coverage: $250,000 to $475,000+. Surety bonds up to $2 million per state depending on volume.

The UK requires FCA authorisation as an Authorised Payment Institution (minimum €125,000 capital) or Electronic Money Institution (€350,000). The timeline is 6 to 12 months, but FCA refusal rates have risen from 1 in 14 in 2021 to 1 in 5 in 2023.

Let me give you the numbers that actually matter.

Custom payment gateway development cost sits across three tiers, and which tier you're in depends on what you're actually developing as your payment gateway.

MVP (3 to 6 months, $150,000 to $250,000): Single market, hosted payment form, basic fraud rules, one acquirer integration. Sufficient for validating the concept and handling early traffic. Not sufficient for enterprise production volumes or multi-market operations.

Production-ready (6 to 12 months, $250,000 to $500,000): Multi-acquirer routing, ML fraud layer, full PCI Level 1 scope, real-time analytics, support for two to three markets. This is where most mid-market clients enter.

Full enterprise (12 to 18+ months, $500,000 to $2,000,000+): Multi-region high availability infrastructure, custom fraud models, six-plus market support, full compliance stack for multiple jurisdictions, embedded analytics, merchant dashboard. This is the tier for businesses where payment infrastructure is a core competitive asset, not just a processing utility.

Here is the component-level breakdown:

Core API Development

Security and Compliance

Bank and Rail Integrations

Fraud Engine Development

UI/UX and Dashboards

QA and Penetration Testing

Infrastructure Setup

Project Management

The costs that most project scopes underestimate:

These hidden costs routinely add 25 to 40% to the headline development estimate. Budget for them explicitly, or encounter them as overruns.

Three trends are reshaping the payment infrastructure landscape right now. Each one has a direct implication for the build vs. buy decision.

FedNow has reached 1,500+ participating financial institutions. It processed $245 billion in Q2 2025 alone, which is 645% year-over-year growth. UPI is live in 8 countries with 30+ in active discussions.

The strategic implication: third-party gateways will lag 12 to 24 months behind custom implementations when new real-time rails emerge in your markets.

Visa has built a platform specifically for AI agents to make payments, partnering with Anthropic, Microsoft, OpenAI, and Stripe. Mastercard completed its first live agentic payment transaction in September 2025.

Gateways not architected for machine-to-machine payment initiation will require significant re-architecture within three to five years.

134 countries are exploring CBDCs. Eleven are fully live. China's e-CNY processes $28 billion a month. UAE's Digital Dirham pilot launched in November 2025. Stablecoin total supply crossed $300 billion in 2025, with September 2025 marking the first month of over $1 trillion in monthly stablecoin transaction volume. Visa's USDC settlement on Solana reached $3.5 billion in annualised run rate within its first quarter.

A custom gateway architecture that treats settlement as a pluggable module can add CBDC and stablecoin rails without re-engineering the core. One hardwired to traditional card clearing cannot.

These trends collectively do one thing to the build vs. buy calculation: they make the long-term cost of inflexibility much higher than it looks today.

Every engagement we take on starts the same way: not with a feature list, but with a compliance-first architecture session.

The regulator you operate under (RBI, CBUAE, FCA, FinCEN) determines your data architecture, your infrastructure geography, and your realistic timeline to market before a single line of code is written. Getting that conversation right at the start is the difference between a 12-month delivery and an 18-month one.

Our delivery follows a structured sequence:

What we bring specifically:

This is most relevant for two types of organisations.

Mid-market businesses processing $5 million to $50 million a month who have outgrown third-party gateways and need a partner who manages both the technical and regulatory complexity.

Enterprise organisations develop a payment gateway as a core competitive asset, where the strategic value of data ownership and checkout control is as important as the fee economics.

If you are scoping a payment gateway for 2026 or 2027, the architecture and compliance decisions you make now determine your timeline, your costs, and your competitive position for the next five years.

Talk to our fintech team. We will give you an honest assessment of your options within a week.

Start your free assessment with the Neuronimbus team.

If you're processing above ~$5 million per month, the limitations of third-party gateways—fees, lack of control, and restricted data access—start becoming expensive. Beyond ~$20 million/month, a custom gateway often makes financial and strategic sense.

No—and thinking that way is shortsighted. Fee savings help, but the real value is owning your payment data, controlling checkout experience, improving authorization rates, and enabling future financial services.

An MVP can take 3–6 months, but a production-ready system typically takes 6–12 months. Enterprise-grade platforms with multi-market compliance and high availability can take 12–18+ months.

Poor architecture decisions—like building a monolith, weak fraud systems, or not owning tokenization—can create long-term scalability, security, and cost problems that are expensive to fix later.

Yes, especially for businesses in the $5M–$20M/month range. It offers more control and flexibility than third-party gateways without the heavy cost and complexity of building from scratch.

.webp)

Let Neuronimbus chart your course to a higher growth trajectory. Drop us a line, we'll get the conversation started.

Call Us

Schedule a Call

Your Next Big Idea or Transforming Your Brand Digitally

Let's talk about how we can make it happen.