If you run technology at a wealth management firm, you already know the pressure is building.

Clients expect a seamless digital experience.

Advisors are buried in manual work.

Legacy systems slow everything down.

And somewhere in the background, a fintech or a digitally native competitor is quietly picking off your next generation of clients.

This performance gap shows up in the numbers.

Deloitte studied 38 US wealth firms and found that the top performers (the ones who had moved furthest on digital transformation in wealth management) were achieving operating margins of nearly 30%, compared to 22% for their peers.

They were also growing AUM and revenue faster. That gap comes from better platforms, better workflows, and better use of data.

The retention risk is just as sharp.

Capgemini found that 81% of inheritors plan to switch wealth management firms within one to two years of inheriting. The number one reason is a mismatch between what clients expect digitally and what firms actually deliver.

Meanwhile, the industry is spending: Celent estimates wealth management IT spend hit $53.7 billion in 2023, on its way to $56.1 billion in 2024, with cloud, automation, and AI as the primary growth areas.

So the investment is happening. The question is whether it is being directed at the right things, in the right sequence, with the right architecture underneath it.

That is what this piece is about.

Also read: AI in Financial Services: Key Insights

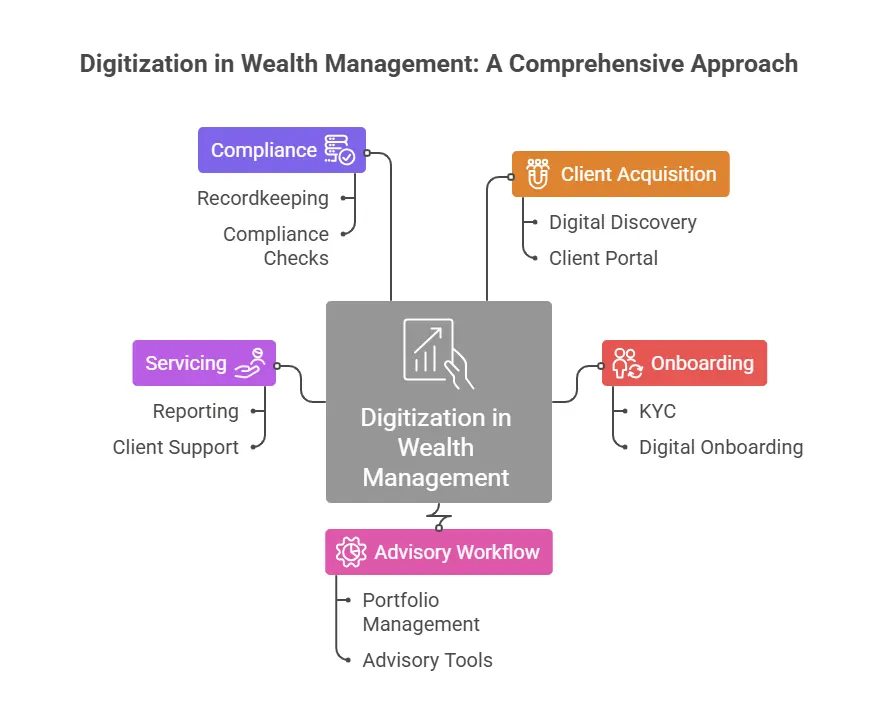

The first thing to understand is that digitization in wealth management is not a front-end project. It is not about building a nicer client portal and calling it done.

It spans the entire value chain:

And yet, in most firms, the digitization effort starts and stops at the client portal.

The underlying workflows are still manual.

The data is still siloed.

Advisors are still spending most of their time doing things that have nothing to do with advising.

AlphaFMC found that relationship managers spend only 30% of their time with clients. Capgemini puts it even more starkly; their research shows RMs spending 67% of their time on non-client-related activities. That means for every hour an advisor works, less than 20 minutes is going toward the thing clients are actually paying for.

That is the real opportunity in wealth management digital transformation.

The question is: what does the technology architecture actually need to look like to close that gap?

This is where most guides on digital transformation in wealth management go vague. They talk about "cloud adoption" and "AI" and "personalization" without ever explaining what the target-state architecture actually looks like or how the pieces connect.

So let us be specific.

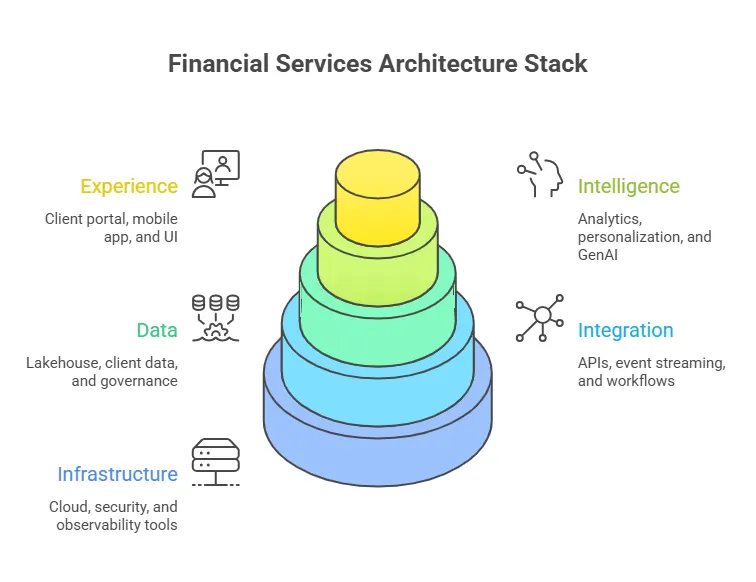

A modern wealth management platform is built in five layers, and they have to work together. If any one layer is weak, it creates a ceiling on what everything above it can do.

What lives here:

Biggest failure mode:

What lives here:

Biggest failure mode:

What lives here:

Biggest failure mode:

What lives here:

Biggest failure mode:

What lives here:

Biggest failure mode:

The experience layer is what clients and advisors see. But it only works as well as the layers beneath it.

A beautiful onboarding interface built on top of a fragmented data layer will still take days to complete because the underlying checks are manual.

A personalization engine that cannot access clean, unified client data will produce generic recommendations.

A GenAI copilot without a governed retrieval layer will hallucinate policy answers and create compliance risk.

The architecture has to be built bottom-up, not top-down.

The integration layer is where wealth management digital transformation most commonly stalls.

Most legacy firms have built integrations point-to-point over many years. When any one of those systems changes, something else breaks. Deployments slow down. Teams spend months maintaining plumbing instead of building value.

The shift to an API-first, event-driven integration layer changes that dynamic. You build the integration once, to a standard, and every system that needs to connect does so through that layer. It is what allows new products, new channels, and new AI capabilities to ship without re-architecting the core.

Celent found that 69% of wealth management firms plan to move more business-critical workloads to public cloud in the next 18 months. That migration only delivers its full value if the integration architecture is cleaned up in parallel. Cloud without API standardisation just moves the mess to a different location.

Here is something that does not get said enough: most firms cannot build the intelligence layer they want because their data layer is not ready for it.

You cannot personalise at scale without clean, unified client data. You cannot run a propensity model on incomplete household data. You cannot give a GenAI copilot reliable answers if the knowledge base it is retrieving from has conflicts and gaps.

This is the hidden cost of deferring the data foundation. And it is the reason many digital transformations in wealth management programs deliver less than they promised.

Fixing this is not glamorous work. But it is the highest-leverage thing a CTO can do before standing up any intelligence layer capability.

The good news is: once the data foundation and integration layer are in place, the use cases that follow move very quickly.

With the architecture foundation in place, the use cases become much more tractable. The question shifts from "can we do this" to "which one do we start with."

Here is what the evidence says about where to begin.

This is the highest-ROI starting point for most firms, and the most direct entry point into improving the wealth management customer journey.

The current state at most firms: onboarding involves paper documents, multiple handoffs, manual identity checks, and a compliance review that can take days or weeks.

Deloitte documented a wealth management cloud modernisation case where the firm achieved a 90% reduction in average intake and onboarding time after platform modernisation. The process went from weeks to hours.

The target state is a standardised digital onboarding pattern built once and reused across channels and product lines.

This single use case, done well, reduces abandonment, compresses cycle time, and creates the compliance logging foundation you will need for everything that comes after.

The second use case follows naturally from the first.

Once data is flowing cleanly through the integration layer, you can give advisors a single view of everything they need: client household data, goals, portfolio drift, pending tasks, communications history, and next-best actions, all in one place, without switching between five systems.

The business case is straightforward. If RMs are spending 67% of their time on non-client activities, and a unified workbench eliminates even a third of that friction, you have effectively expanded advisor capacity without hiring. For a firm with 200 advisors, that is a material productivity gain.

This is also where wealth manager digital transformation creates a compounding effect. Advisors who spend more time with clients retain more clients. Retained clients refer to more clients. The technology investment pays back through the revenue line, not just the cost line.

This is where most of the current industry excitement is focused, and for good reason.

McKinsey found that more than 62% of independent advisors intended to use some form of AI in wealth management for efficiency purposes, versus only around 20% for client-facing tasks. That sequencing is not just a preference. It is the right strategy.

Starting with an internal copilot delivers value quickly while keeping regulatory risk manageable. The model is not talking to clients. It is helping advisors prepare better for the conversations they are already having.

The technical requirement is a governed retrieval layer. The copilot should be pulling answers from approved, version-controlled internal content, not generating answers from the open internet. Every prompt and output should be logged. Role-based access should control what each user can ask. And there must be a clear human-in-the-loop escalation path for anything the model is not confident about.

Celent found that 60% of wealth firms are already live, piloting, or experimenting with GenAI. Governance is not optional at this stage. It is the thing that determines whether the rollout accelerates or gets shut down by compliance.

Once the data layer is clean and the advisor workbench is running, personalisation becomes achievable at scale.

The use case is: segment clients by behaviour and life stage, model propensity for specific products or conversations, and surface next-best actions to advisors at the right moment. Not generic. Not rule-based. Actually driven by what the data says about that specific household.

This is directly connected to the retention problem. If 81% of inheritors are planning to leave their current firm, the firms that retain them will be the ones that made them feel understood; that reached out at the right moment, with the right message, about the right product. Personalisation at scale is how you do that with 500 clients per advisor instead of 50.

No honest treatment of wealth management digital transformation is complete without covering what actually derails these programs.

The regulatory environment in the US is demanding and getting more so. The SEC's amendments to Regulation S-P, effective August 2024, require firms to maintain incident response programs designed to detect, respond to, and recover from unauthorized access to customer information. That is not a legal footnote. It is an architecture requirement.

Recordkeeping is another live risk. The SEC's FY2024 enforcement results included more than $600 million in civil penalties related to recordkeeping cases, and over $2 billion since December 2021 across the broader initiative. If your digital platform is generating communications, those records have to be captured, retained, and retrievable.

On the AI side, the FCA has stated it will not introduce AI-specific regulation, instead relying on existing frameworks. That sounds like relief but it is not. It means your existing governance obligations fully apply to whatever your AI systems do. The FCA has been explicit about needing stronger testing, validation, explainability, and accountable ownership as AI complexity increases.

And then there is the execution risk that has nothing to do with technology. Deloitte estimates 70% of digital transformations fail. The cause is almost never the platform. It is change management.

Build the governance in. Measure outcomes from day one. Assign a business owner to every use case, not just a project manager.

Everything described above, such as the architecture layers, the use case sequencing, the compliance requirements, the data foundations, is exactly the territory Neuronimbus operates in.

We work with wealth management technology teams at the intersection of platform modernisation, integration engineering, data foundations, and governed AI enablement. Not as a software vendor. As the execution partner that takes a firm from "we know we need to transform" to "we have a working platform and a clear roadmap."

Our engagement model is designed to reduce risk and deliver early value:

The 90-day MVP model matters because it creates proof of value before you are asking for a multi-year commitment. It also forces the architectural decisions that will determine how fast everything after it can move.

If you are mapping your transformation roadmap for 2025–2026, the right starting point is a conversation about your current stack and where the real friction is.

Digital transformation in wealth management is the use of modern technologies such as cloud, APIs, automation, AI, and data platforms to improve client onboarding, advisor productivity, portfolio management, compliance, and overall customer experience.

Digital transformation helps wealth management firms reduce manual work, improve advisor efficiency, deliver better client experiences, and stay competitive against fintech and digitally advanced firms. It also supports faster growth in AUM, revenue, and client retention.

The most common use cases include digital onboarding and eKYC automation, unified advisor workbenches, GenAI advisor copilots, personalized client engagement, next-best-action recommendations, and automated compliance and reporting workflows.

A modern wealth management architecture typically includes five layers: experience layer, intelligence layer, data layer, integration layer, and infrastructure layer. Together, these layers enable seamless digital experiences, automation, analytics, and governed AI adoption.

The biggest challenges include legacy systems, siloed data, poor integration, compliance and recordkeeping requirements, AI governance risks, and change management. Firms often struggle when they invest in front-end tools without fixing data and architecture foundations first.

.webp)

Let Neuronimbus chart your course to a higher growth trajectory. Drop us a line, we'll get the conversation started.

Call Us

Schedule a Call

Your Next Big Idea or Transforming Your Brand Digitally

Let's talk about how we can make it happen.